Dear Clients and Friends,

We hope each of you are enjoying the beginning of summer. Here in Colorado, our snow-capped peaks stand proudly against a backdrop of vibrant greenery, creating a beautiful contrast that usually only lasts for a few weeks.

In this month's newsletter, we will be talking about macro trends, specifically how inflation, the economy, and markets are doing based upon recent data and how this is impacting our portfolios.

Market Overview

The trade deficit marked lower in April, meaning U.S. exports were higher for the month relative to imports. Inflation also slowed sharply with the Federal Reserve’s preferred measure of inflation now up only 2.1% on a year-ago comparison basis, just a hair above the official target of 2.0%.

Investors are understandably confused. After real GDP declined at a 0.2% annual rate in the first quarter, many thought this dip was a harbinger of recession, with more declining real GDP ahead.

But what is becoming clear now is the decline in Q1 real GDP was largely due to an unprecedented surge in imports (front-running tariffs), and that will likely reverse in Q2 and beyond.

None of this means we are out of the woods on recession risk or that the inflation dragon has been slain. If the Fed were to dramatically loosen monetary policy, inflation could come back quickly, and there are plenty of reasons why a recession could still happen. The U.S. recession probability indicator still remains elevated at 30+%.

But in general, we are pleased with the stock market largely recovering from the sharp downward movements in February, March, and April and remain optimistic that innovative technology will continue to catalyze markets higher alongside a growing economy and controlled inflation.

Key Trends Shaping Your Portfolio

While the volatility in the stock market has remained elevated, there is growing momentum to the upside and consistent buying demand when prices push lower. As of this writing the main indices are approximately as follows:

S&P 500: 1%

Nasdaq 100: 0.75%

Russell 2,000: -6%

While markets have regained ground, valuations remain high amongst the largest names in the top indices. In other words, mega-cap technology companies are demanding a higher share price per level of earnings or book value than smaller sized companies in the S&P 500. If earnings do not keep up with these higher valuations, then a reversion to the mean is likely.

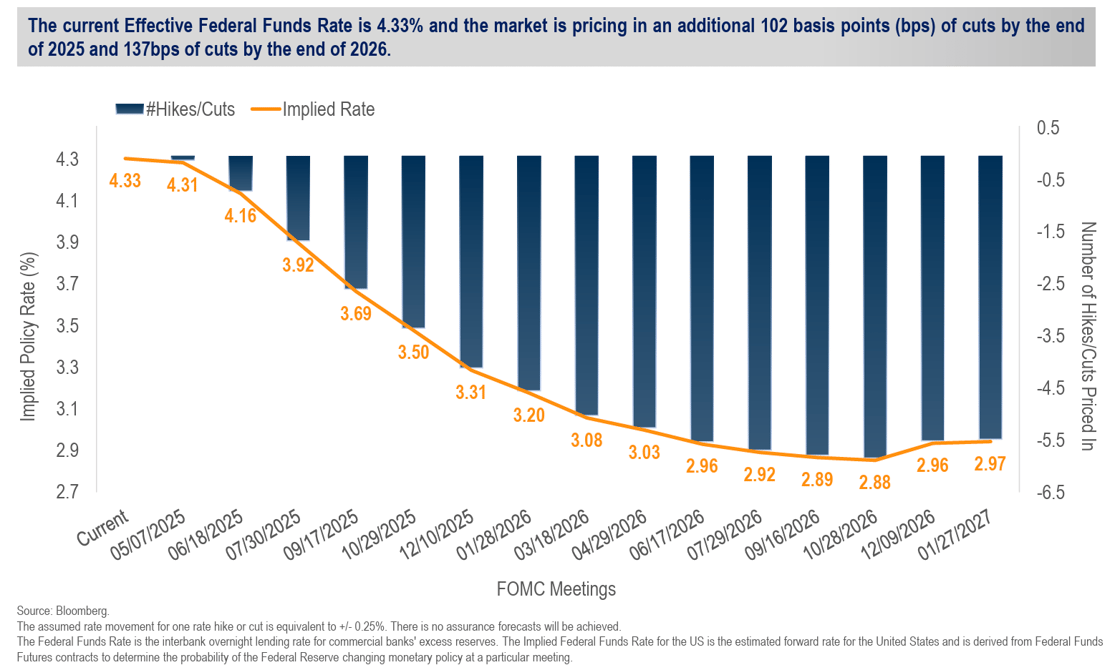

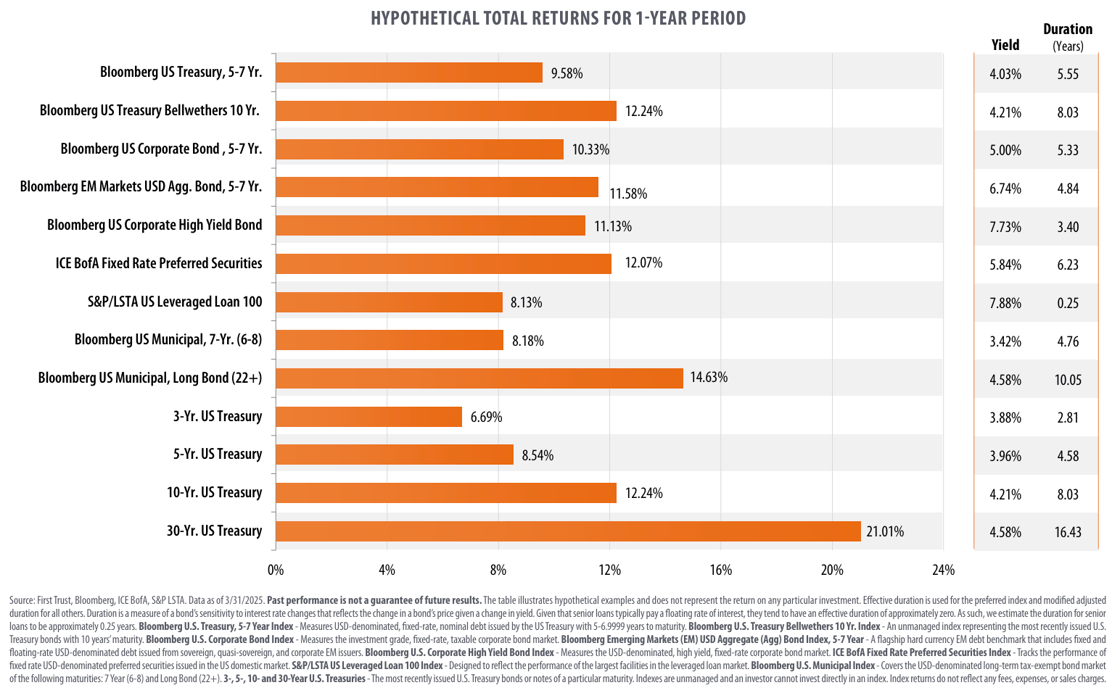

The bond market has been the most surprising this year with a seesaw in rates that has caused prices to be more volatile. As of 4/30/2025 the market is pricing in about a -1% reduction in rates by the end of the year.

If this occurs, bond prices should go up in response and housing activity also accelerate.

Asymmetry is also back in the bond market where rate increases have a modest negative impact on prices, but rate decreases have a magnified impact on prices, illustrated below:

Investment Strategy and Outlook

Our outlook for 2025 emphasizes diversification and agility. We will maintain broad exposure to international and domestic stocks with slight overweights into sectors we believe are well positioned for the current environment.

We are cautiously optimistic about U.S. corporate earnings, but remain ready if valuations at the top of the index get stretched too thin.

Our bond portfolios are well positioned to take advantage of the current asymmetry and we remain vigilant to find yield through structured notes and outperformance through private markets.

Looking Ahead

Over the summer months we will be reviewing your estate plans/documents/beneficiaries as well as reviewing investments and running stress tests.

We invite you to schedule a consultation to review your portfolio and discuss these items. Thank you for your continued trust in us as your wealth management partner.

Warm regards,

The Bauer Heitzmann Team

.png)